A Mixed Quarter for Interest Rates, but Credit Continues Its Rally

The third quarter in bond funds.

/s3.amazonaws.com/arc-authors/morningstar/bc7d88a3-8cc9-454a-994a-b769dee12e69.jpg)

All eyes were once again on the Federal Reserve in the third quarter. Although the Fed didn't hike, the broader rates environment was mixed. Perhaps the biggest story of the quarter was the continued rally in credit-sensitive bonds.

Rates, Rates, and More Rates The Fed once again made news in July and September with its decision not to raise short-term policy rates. In her speech following the September decision, Fed Chair Janet Yellen noted that economic conditions had strengthened since the first half of the year, signaling an openness to a potential hike later in the year. There were other signs that a hike might be on the table in December, including dissents from three Federal Reserve regional bank heads. As of Wednesday, the Fed Funds futures markets were pricing in a bit more than a 50% chance of a rate increase by December.

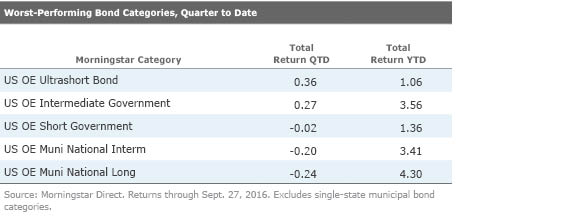

Despite the Fed's inaction, bond yields increased across most maturities during the third quarter to date before bouncing back in the final weeks of the quarter. Yields on the 10-year Treasury note bottomed at 1.37% in early July and got as high as 1.73% on Sept. 13 before falling again to 1.56% as of Sept. 27. That increase in yields and a strong supply of new issuance in the municipal market meant modest losses for some muni categories. That said, the modest backup in yields during the quarter hasn't had a meaningful impact on what's still been an impressive run for longer-maturity bond funds so far in 2016.

Libor was also on the rise during the quarter. Libor rates, which are widely used as a global benchmark for variable-rate loans, had been moribund for much of 2014 and 2015 before spiking at the beginning of 2016 and once again during the third quarter. As PIMCO's Jerome Schneider explained in a recent video, one of the biggest drivers of the increase in Libor is the looming implementation of money market regulations. Assets have surged out of prime money market funds, thus lowering demand for the certificates of deposit and commercial paper that many financial institutions use for funding. That has created opportunities for ultrashort- and short-term bond funds, including

The Tremendous Rally in Credit Continued Since oil prices bottomed on Feb. 11, credit markets have enjoyed eye-popping gains with returns on the major high-yield indexes of roughly 20%, a touch above the return on the S&P 500 during the period. That trend continued into the third quarter as the convertibles and high-yield bond categories were poised to come out tops among U.S. fixed-income categories. The gains were more muted in investment-grade credit, although the corporate sector was once again the strongest-performing sector within the recently renamed Barclays Bloomberg U.S. Aggregate Bond Index, providing support for that benchmark's relatively modest 0.7% gain for the quarter through Sept. 27; the typical intermediate-term bond fund was up a little more than 1% during the period, and funds with large corporate stakes did particularly well.

Within high yield, funds with large allocations to energy have prospered. Energy bonds, which bore the brunt of 2015 losses together with metals and mining related names, have seen a surge in defaults, but the energy sector of the high-yield index has rebounded sharply from lows suffered earlier this year.

Emerging-Markets Debt Is Still a Top Performer After enduring three straight years of losses driven largely by struggles in local-currency debt and corporates, emerging-markets bond funds have been big winners so far in 2016. Despite Moody's and S&P's downgrade of Turkey's debt rating to below-investment-grade, that performance continued into the third quarter. The lack of a rate hike in the Unied States and a stabilization in commodity prices all helped buoy returns, especially in Latin America. Indeed, the emerging-markets bond Morningstar Category, which includes funds that typically hold a significant stake in dollar-denominated emerging-markets debt, was the second-best-performing category for the quarter to date. Both that category and the emerging-markets local-currency bond category, which includes funds focused on local-currency bonds from emerging-markets issuers, were among the top performers for the year to date. A rebound in Brazilian local-currency debt after a terrible 2015 was a bright spot for funds in the latter category.

While positions in emerging-markets debt have helped funds with large allocations to the sector; one exception was

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NPR5K52H6ZFOBAXCTPCEOIQTM4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OMVK3XQEVFDRHGPHSQPIBDENQE.jpg)

/d10o6nnig0wrdw.cloudfront.net/09-24-2024/t_c34615412a994d3494385dd68d74e4aa_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/bc7d88a3-8cc9-454a-994a-b769dee12e69.jpg)